With a Personal Injury Earnings Loss claim where the claimant has an Ill-health Pension and is also able to continue working (and so has Actual Earnings) then be very careful how those Actual Earnings are calculated – there may be a significant impact on lost earnings.

When a claimant has an Ill-Health Pension, we know from Parry v Cleaver (1970) AC1 that this pension income is not to be deducted from their But For income prior to their Normal Retirement Age (“NRA”).

Rather, the ill-health pension is set against their But For pension, thereby reducing their pension loss:

Ok, that’s simple enough BUT there can be a ‘twist’ with identifying what the claimant’s Actual Earnings are when there is an ill-health pension in payment.

Let’s look at Sarah’s claim

Sarah was active in the Army Cadets at school where she excelled academically. She went on to Uni and gained a First-Class degree in electrical engineering before then joining the Armed Forces. Sarah was doing well in her forces career (she had reached the rank of Major and was on course to end her military career as a Brigadier) but unfortunately was badly injured in an accident in 2018, aged 40. Sarah was medically discharged from the Forces in 2020.

But For injury Sarah had planned to stay in the forces until age 55 and then pursue a second career in the private defence sector. Fortunately for Sarah, her skills and experience meant that she quickly secured a well-paid civilian job, as an electronics engineer, on a salary of £100,000.

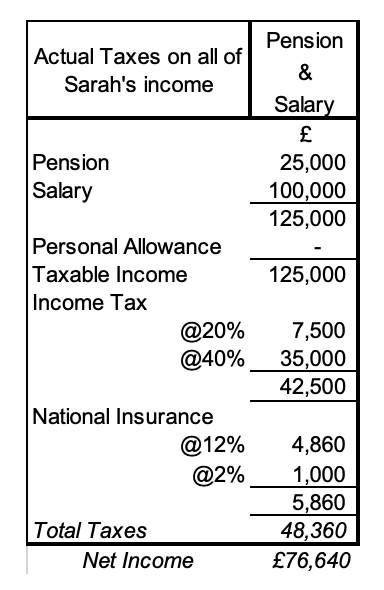

Keeping the numbers relatively simple, in the year ended 31 March 2021 Sarah’s total gross income was £125,000, which came from her Armed Forces pension of £25,000 plus her Civilian Salary of £100,000. So, for the 2021 tax year, Sarah’s actual net of taxes income was £76,640:

If we look at the above calculation of her Net Income. Sarah’s income (comprising Pension & Salary) was above the Personal Allowance limit for 2021 of £125,000, meaning that she got no personal tax allowance set-off against her income and her income was then taxed at 20% & 40%, plus Class 1 National Insurance contributions on her salary (but not her pension) income.

Now, we know that Parry v Cleaver tells us not to deduct the Ill-Health pension until after Sarah’s Normal Retirement Age. That would be her normal discharge date from the Armed Forces of aged 55. OK – that’s simple, got that!

So, we now have to calculate Sarah’s lost earnings (for the 13 years 2020 to 2033 when she is aged 55 and reached her Forces NRD). To do this we need to compare Sarah’s But For Injury Armed Forces Earnings with her Actual With Injury Civilian Earnings, for each year until she is 55.

The big question is – how (set against Parry v Cleaver) should we calculate Sarah’s after-tax Civilian Engineer’s earnings, when she is at the same time in receipt of (and taxed on!) her ill-health pension income?

Well, there are different ways of calculating Sarah’s Net (salary) Income – and they give wildly varying answers! I have just spent some time arguing what is a fair and reasonable approach in these circumstances.

Let’s take a look at two ways of calculating Sarah’s after-tax civilian salary

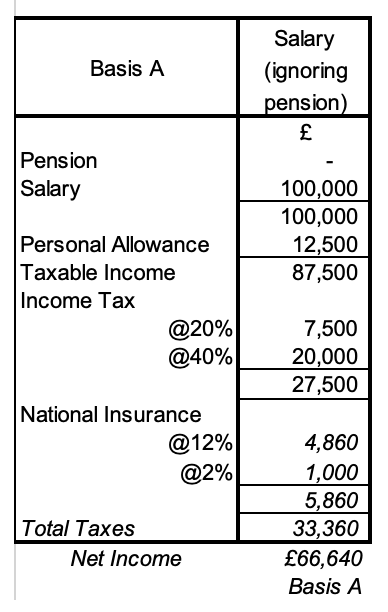

First method: Let’s ignore the Pension and pretend that the Civilian Salary is all that exists, let us call this Basis A. This calculation method produces a Net Earnings figure for Sarah of £66,640:

That was the method used by the Defendant’s accountancy expert, who asserted that Parry v Cleaver meant that one should ignore the ill-health pension, simply ‘pretend’ it does not exist.

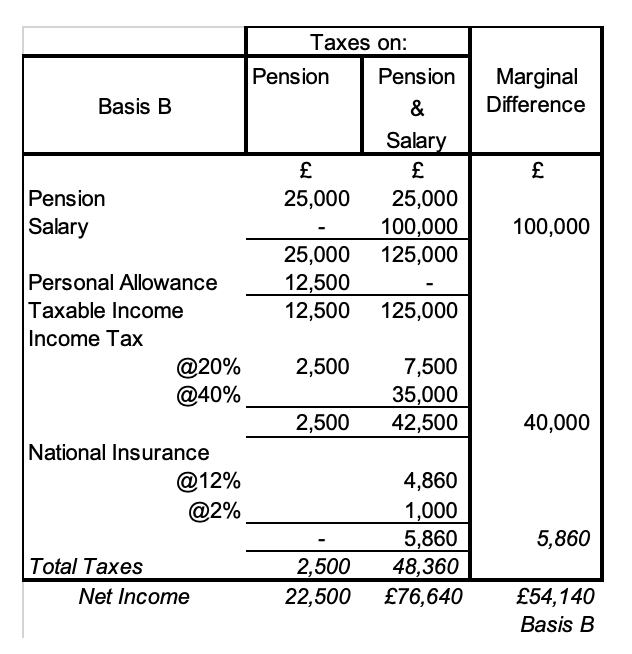

Second method: let us look at the marginal impact the salary has on Sarah’s net income

The Sarah is mitigating her lost Armed Forces salary by working in the civilian sector and generating alternative income, which is in addition to her Armed Forces Ill-health pension. The reality is that Sarah receives an Armed Forces Ill-health pension and in parallel works in her civilian job to mitigate her personal injury losses – and again the reality is that Sarah pays ‘taxes’ arising from both her pension and salary incomes.

To identify the marginal impact of the Civilian salary, income that is additional to her Armed Forces pension, we calculate the taxes arising on just the pension and compare these with the taxes arising on both the pension and salary. This is our second (basis B) method. The difference equates directly to the marginal impact of the salary. On Basis B we arrive at Net Earnings (based on Sarah’s Civilian Salary) of £54,140, which is much less Basis A – where Sarah’s earnings are calculated on the Civilian Salary in isolation:

The Actual Net Income from Sarah’s Civilian Job will be deducted from her But For Net Income (from her Armed Forces Job) so as to identify her lost earnings. As such, it is (I would say, very) material that there is a 23% difference in Actual Net Income between the A & B calculation bases. Ignoring discounting and uncertainty adjustments, over 13 years the difference in the two calculation methods (A & B) is a staggering £162,500.

The story doesn’t end there, as there are other potential ways one could estimate the taxes attributable to the Civilian Salary.

For example, one could identify the top slice of taxes in 2021 and attribute that to the salary or one could ‘simply’ pro-rata the actual total tax bill for 2021 between pension and salary incomes. I don’t like either of these methods; I feel they are somewhat artificial and theoretical. That is particularly, when those methods are compared against Basis B – which identifies the real financial impact of Sarah’s Civilian Salary ‘arriving’ in addition to her Armed Forces Pension.

The takeaway from this story is be aware that when there is an ill-health pension and the claimant is capable of working then be mindful that the way taxes are calculated can impact (potentially significantly) on Earnings Loss Quantum.

We are always happy to give initial thoughts & advice on evidence and approach to loss quantum. Contact us today Richard@FormbyForensics.co.uk or tel. 01761- 437972

Formby Forensic Services Personal, friendly, service – years of experience – prompt attention and turnaround

76 Comments

Personal Injury Loss Quantum: Pensions – huge value, lots of issues, not to be taken lightly! - Formby Forensics · 14 July 2023 at

[…] advice if you have a case with these components. If you want an illustration – see an earlier blog I wrote on this topic about on Parry V Cleaver, a twist to watch out […]

does viagra make your dick bigger · 20 December 2024 at

does viagra make your dick bigger

does viagra make your dick bigger

longs pharmacy store locator · 20 December 2024 at

longs pharmacy store locator

longs pharmacy store locator

liquid vardenafil dosage · 20 December 2024 at

liquid vardenafil dosage

liquid vardenafil dosage

levitra generic cheap · 20 December 2024 at

levitra generic cheap

levitra generic cheap

bluechew tadalafil review · 20 December 2024 at

bluechew tadalafil review

bluechew tadalafil review

sildenafil directions · 21 December 2024 at

sildenafil directions

sildenafil directions

sildenafil citrate 100mg · 21 December 2024 at

sildenafil citrate 100mg

sildenafil citrate 100mg

sildenafil citrate over the counter · 21 December 2024 at

sildenafil citrate over the counter

sildenafil citrate over the counter

sildenafil 100mg efectos secundarios · 21 December 2024 at

sildenafil 100mg efectos secundarios

sildenafil 100mg efectos secundarios

sildenafil warnings · 21 December 2024 at

sildenafil warnings

sildenafil warnings

can i get misoprostol at a pharmacy · 22 December 2024 at

can i get misoprostol at a pharmacy

can i get misoprostol at a pharmacy

levitra online sale · 22 December 2024 at

levitra online sale

levitra online sale

does cialis keep you hard after coming · 22 December 2024 at

does cialis keep you hard after coming

does cialis keep you hard after coming

how does levitra work · 23 December 2024 at

how does levitra work

how does levitra work

tadalafil 6mg chewable · 23 December 2024 at

tadalafil 6mg chewable

tadalafil 6mg chewable

tadalafil over the counter · 23 December 2024 at

tadalafil over the counter

tadalafil over the counter

levitra 10mg online · 23 December 2024 at

levitra 10mg online

levitra 10mg online

pharmacy viagra online · 23 December 2024 at

pharmacy viagra online

pharmacy viagra online

sildenafil 100mg en español · 23 December 2024 at

sildenafil 100mg en español

sildenafil 100mg en español

cheap levitra online · 23 December 2024 at

cheap levitra online

cheap levitra online

viagra vs cialis which is better · 24 December 2024 at

viagra vs cialis which is better

viagra vs cialis which is better

propecia discount pharmacy · 24 December 2024 at

propecia discount pharmacy

propecia discount pharmacy

sildenafil 100mg · 24 December 2024 at

sildenafil 100mg

sildenafil 100mg

pre pharmacy courses online · 24 December 2024 at

pre pharmacy courses online

pre pharmacy courses online

what is vardenafil hcl used for · 24 December 2024 at

what is vardenafil hcl used for

what is vardenafil hcl used for

sildenafil 45 mg · 24 December 2024 at

sildenafil 45 mg

sildenafil 45 mg

periactin online pharmacy no prescription · 24 December 2024 at

periactin online pharmacy no prescription

periactin online pharmacy no prescription

online pharmacy no prescription lexapro · 25 December 2024 at

online pharmacy no prescription lexapro

online pharmacy no prescription lexapro

hydrochlorothiazide online pharmacy · 25 December 2024 at

hydrochlorothiazide online pharmacy

hydrochlorothiazide online pharmacy

vardenafil tablet · 25 December 2024 at

vardenafil tablet

vardenafil tablet

online pharmacy no prescription needed tramadol · 25 December 2024 at

online pharmacy no prescription needed tramadol

online pharmacy no prescription needed tramadol

tadalafil 20mg for premature ejaculation · 25 December 2024 at

tadalafil 20mg for premature ejaculation

tadalafil 20mg for premature ejaculation

misoprostol pharmacy cost · 25 December 2024 at

misoprostol pharmacy cost

misoprostol pharmacy cost

is tadalafil stronger than sildenafil · 25 December 2024 at

is tadalafil stronger than sildenafil

is tadalafil stronger than sildenafil

tadalafil 20 mg para que sirve · 25 December 2024 at

tadalafil 20 mg para que sirve

tadalafil 20 mg para que sirve

tadalafil warnings · 25 December 2024 at

tadalafil warnings

tadalafil warnings

how long is tadalafil effective · 25 December 2024 at

how long is tadalafil effective

how long is tadalafil effective

tijuana pharmacy oxycodone · 25 December 2024 at

tijuana pharmacy oxycodone

tijuana pharmacy oxycodone

celebrex inflammation dosage · 27 December 2024 at

celebrex inflammation dosage

celebrex inflammation dosage

tegretol dda · 27 December 2024 at

tegretol dda

tegretol dda

carbamazepine dosage for adults · 27 December 2024 at

carbamazepine dosage for adults

carbamazepine dosage for adults

para que sirve celecoxib 200 · 27 December 2024 at

para que sirve celecoxib 200

para que sirve celecoxib 200

etodolac efectos adversos · 27 December 2024 at

etodolac efectos adversos

etodolac efectos adversos

gabapentin dogs · 27 December 2024 at

gabapentin dogs

gabapentin dogs

gabapentin osteopenia · 28 December 2024 at

gabapentin osteopenia

gabapentin osteopenia

can amoxicillin and ibuprofen be taken together · 28 December 2024 at

can amoxicillin and ibuprofen be taken together

can amoxicillin and ibuprofen be taken together

sulfasalazine loss appetite · 28 December 2024 at

sulfasalazine loss appetite

sulfasalazine loss appetite

can you drink alcohol while taking motrin 800 · 28 December 2024 at

can you drink alcohol while taking motrin 800

can you drink alcohol while taking motrin 800

what side effects does elavil have · 30 December 2024 at

what side effects does elavil have

what side effects does elavil have

amitriptyline for pain dose · 30 December 2024 at

amitriptyline for pain dose

amitriptyline for pain dose

cilostazol preço rj · 30 December 2024 at

cilostazol preço rj

cilostazol preço rj

mestinon reacciones adversas · 30 December 2024 at

mestinon reacciones adversas

mestinon reacciones adversas

oxaprozin vs indomethacin · 30 December 2024 at

oxaprozin vs indomethacin

oxaprozin vs indomethacin

imitrex injection maximum dose · 30 December 2024 at

imitrex injection maximum dose

imitrex injection maximum dose

interactions with mebeverine · 31 December 2024 at

interactions with mebeverine

interactions with mebeverine

can i order cheap pyridostigmine · 31 December 2024 at

can i order cheap pyridostigmine

can i order cheap pyridostigmine

diclofenac high feeling · 31 December 2024 at

diclofenac high feeling

diclofenac high feeling

imdur blood pressure · 7 January 2025 at

imdur blood pressure

imdur blood pressure

15 mg mobic dosage · 7 January 2025 at

15 mg mobic dosage

15 mg mobic dosage

imuran drug study · 7 January 2025 at

imuran drug study

imuran drug study

sumatriptan succinate imigran · 7 January 2025 at

sumatriptan succinate imigran

sumatriptan succinate imigran

generic for rizatriptan benzoate · 7 January 2025 at

generic for rizatriptan benzoate

generic for rizatriptan benzoate

intrathecal baclofen therapy benefits and complications · 7 January 2025 at

intrathecal baclofen therapy benefits and complications

intrathecal baclofen therapy benefits and complications

lioresal 10 mg bijsluiter · 7 January 2025 at

lioresal 10 mg bijsluiter

lioresal 10 mg bijsluiter

difference between 6-mp and azathioprine · 7 January 2025 at

difference between 6-mp and azathioprine

difference between 6-mp and azathioprine

piroxicam plasma protein binding · 8 January 2025 at

piroxicam plasma protein binding

piroxicam plasma protein binding

can you get high off of meloxicam 7.5 mg tabs · 8 January 2025 at

can you get high off of meloxicam 7.5 mg tabs

can you get high off of meloxicam 7.5 mg tabs

maxalt prospektüs bilgileri · 8 January 2025 at

maxalt prospektüs bilgileri

maxalt prospektüs bilgileri

tizanidine rash · 9 January 2025 at

tizanidine rash

tizanidine rash

can i buy generic toradol without dr prescription · 9 January 2025 at

can i buy generic toradol without dr prescription

can i buy generic toradol without dr prescription

cyproheptadine mnemonic · 9 January 2025 at

cyproheptadine mnemonic

cyproheptadine mnemonic

purchase periactin appetite stimulant · 9 January 2025 at

purchase periactin appetite stimulant

purchase periactin appetite stimulant

can you buy generic ketorolac without insurance · 9 January 2025 at

can you buy generic ketorolac without insurance

can you buy generic ketorolac without insurance

02 shop artane castle · 9 January 2025 at

02 shop artane castle

02 shop artane castle

difference between zanaflex capsules and tablets · 9 January 2025 at

difference between zanaflex capsules and tablets

difference between zanaflex capsules and tablets

Comments are closed.